How the Bank of England rate drop effects your mortgage:

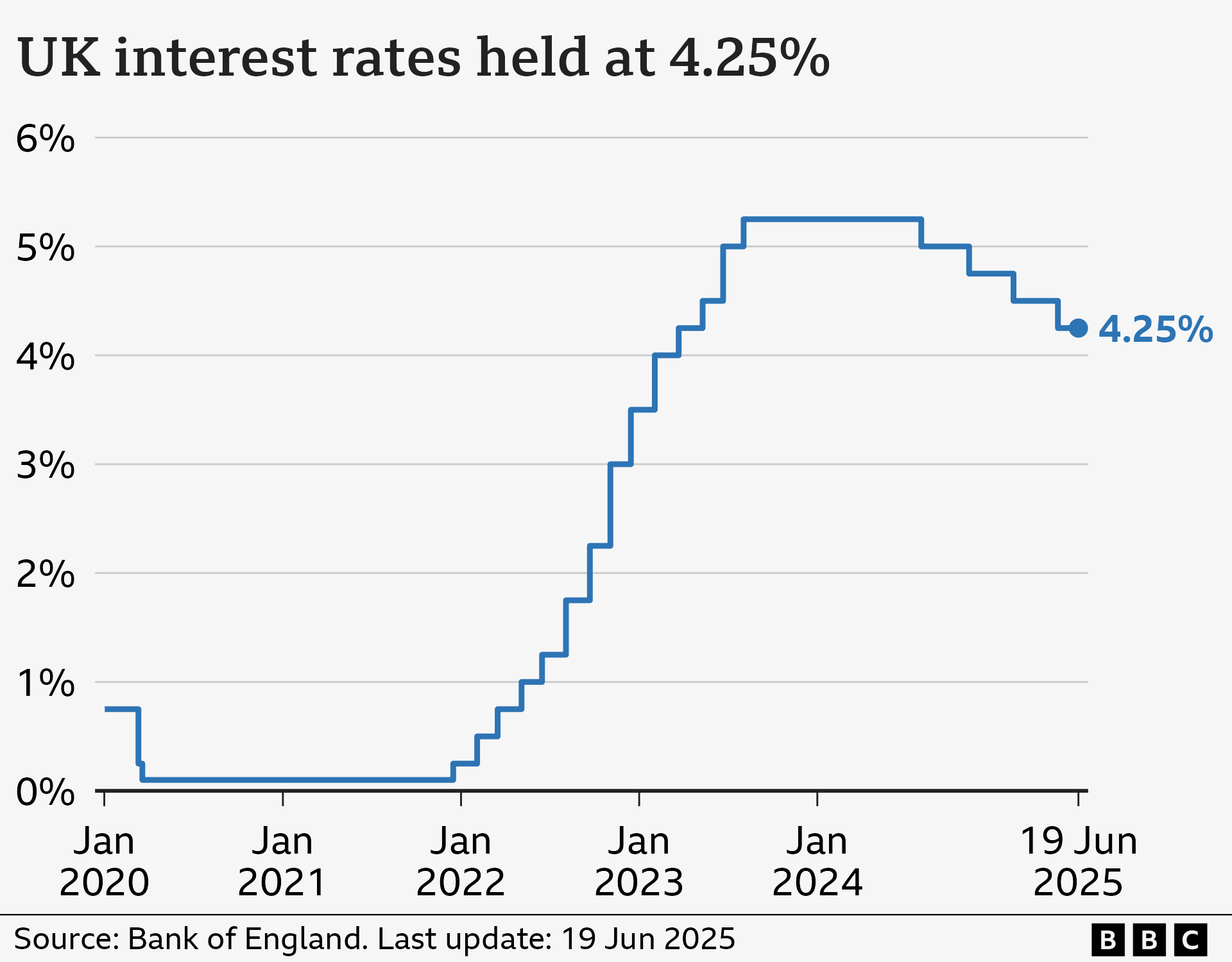

Update (18 December 2025): The Bank of England has cut the Bank Rate by 0.25% to 3.75%, following a tight 5–4 vote.

Depending on your mortgage position, this will play out differently for you. If you are on a tracker mortgage, you may feel the change quite quickly and will receive notification from your lender that your rate will reduce at a set date. This is because a tracker mortgage rate follows the Bank of England base rate plus a specific lender added margin (e.g., Base + 0.75%).

If you are on a fixed rate you will have no change to your rate or your monthly payments. However, if you want to review your fixed rate, it maybe that you are within the right timeframe to remortgage, or if you have no ERC (early repayment charge to end the mortgage), you can assess your options. Though an interest rate change, doesn’t suddenly change all individual mortgage lender rates.

For BTL Landlords, a small shift can alter the numbers across an individual or multiple properties.

Regarding the backdrop, inflation has eased, with CPI reported at 3.2% in November, down from 3.6% in October. Inflation falling, doesn’t mean things are getting cheaper, it just means the price rises are going at a slower pace.

The headline: Base rate down to 3.75%.

The reality: Mortgage rates do not all drop overnight, and not all lenders move at the same speed.

The Bank of England has reduced the base rate today. That headline matters, but what you do next depends on your mortgage type, your timeline, and whether you are managing one mortgage or a whole portfolio.

Some people will feel the impact quickly and others won’t see any change at all until their deal ends. Either way, this rate move is a clear signal that the pricing mood is shifting which is positive.

The big takeaway: a base rate cut can help, but it does not instantly rewrite every mortgage rate. The right move is to check where you are now and line up options early if you’re close to renewal.

More Detail of what changes now (and what doesn’t)

- Tracker mortgages: often move in line with base rate (check your product terms). SVR and lender variable rates: can change, but it’s the lender’s call. The base rate cut doesn’t force an automatic drop.

- Fixed rates: your current payment stays the same until your fixed period ends.

- New deals: lenders may reprice and compete, but it’s rarely instant and it can be patchy across the market. It is important to ensure you compare the market and assess the right mortgage options for your circumstances.

If you are on a tracker or variable rate

This is where you are most likely to see a difference sooner rather than later. Even so, don’t assume you are on the most competitive option just because your rate moves with base rate. Some trackers are sharp, others are expensive and it’s important to review the wider market options and not just your current lender. SVR in particular can stay stubbornly high compared to what is available elsewhere.

If your fixed deal ends in the next 6 months

Waiting until the last minute usually means fewer choices and more pressure, whereas reviewing early means you can lock in any rates to secure them, but still shift to a lower rate as they become available. With the help of an independent mortgage broker, you can compare thousands of products, line up a switch early and keep it under review if lenders cut pricing again.

Practical point: you can still switch before 31 December 2025 or, at the very least, get your options compared and a plan in place for early 2026.

Portfolio landlords: why this matters across your whole book

If you are running a portfolio, the impact isn’t just “one payment” of course – it is an accumulative margin differentiator. Your rate change of course can influence various aspects of your situation, such as:

- Portfolio cashflow and interest cover

- Affordability and stress testing on refinances

- Whether a product transfer stacks up versus a remortgage

- Timing decisions across multiple product end dates

Even if you are not refinancing today, it’s worth mapping what’s due in the next 6–12 months so you’re making moves on your terms, not your lender’s.

Working with The Mortgage Broker, you can utilise our mortgage monitoring app, and have all your property rates monitored 24/7, with notifications across each one when options may improve or the time to review occurs.

Fixed vs tracker: a quick comparison

A fixed rate buys you payment certainty. A tracker can benefit when rates fall, but your payment can move around and you will feel any future increases too. Neither is “best” in isolation, but rather it comes down to how you budget, how long you plan to keep the mortgage, and how much change you are comfortable with. Along with your risk appetite of course.

We’ve covered this properly here : Should you fix or track your mortgage? Navigating rate choices

Want to see what today’s cut means for you?

Compare rates across our panel of 130+ lenders and thousands of options, then decide whether switching could reduce your monthly payment or improve your longer term plan.

Call: ![]() 0800 0320 316

0800 0320 316

Your home may be repossessed if you do not keep up repayments on your mortgage.

Sources: The Independent live updates, BBC and Reuters report on the decision.